By Joaquín Bossie, Co-founder & CRO at Minders

By Joaquín Bossie, Co-founder & CRO at Minders

The average Argentine adult has more than 7 financial accounts. According to COELSA, there are 262 million active accounts in the country.

In that context, there’s only one question that should sit at the center of every product meeting: which one do they tap into every morning?

That’s the race for primacy. And after working with more than 70 clients in the financial sector across Latin America, we’ve started to see clearly what separates the fintechs that win it from the rest.

Acquisition and primacy are different things

The Argentine fintech sector has been going through years of accelerated growth. Electronic payments increased 45% year-over-year. Adults make an average of 28 payments per month. Today, almost any user has access to a digital financial product. The challenge is no longer acquisition — it’s moved on to something harder: getting people to choose you every single day.

Primacy means being the app the user opens first. The one they use when they need to pay for something important. The one that lives on their home screen because they chose it, not because they downloaded it once for a promo.

What builds that habit is simple to say and hard to execute: get the user to come back tomorrow. And the day after. And next month.

Three things the fintechs that win do differently

What we see in companies that build primacy is that they don’t necessarily have the best product or the biggest marketing budget. They have three habits that set them apart.

1. They measure what matters

Companies that win measure retention at 30, 60, and 90 days. They measure usage frequency product by product — understanding who the user is that pays, where they pay, how they pay, which feature they use, when they take out a loan, when they pay it back, and when they return to the app. And they measure incremental revenue — the revenue their actions actually generated, not the total. They don’t look at installs or opens. They look at business metrics that truly impact what matters. Those are the ones that tell you whether a product is building habit or just accumulating sign-ups.

2. They experiment on everything

Experimentation is a process: first measure the problem and understand it, then generate a hypothesis, define the concrete objective of what you want to implement, and only then launch — so you can measure whether you’re actually generating impact or whether the results would have happened anyway.

Companies that build primacy have this discipline embedded in their operations. Every campaign has a holdout group. Every new feature gets validated before scaling. And the speed of learning — more than the speed of execution — is one of the most important competitive advantages in this environment.

One data point I think is worth sharing: only 30% of campaigns generate real incrementality. That’s exactly why you need to experiment a lot and learn fast.

3. They personalize with intention

When I talk about personalization, we can’t stop at putting someone’s name in an email anymore. I mean making at least nine decisions per user: who you’re sending the message to, which channel, at what moment, with what tone, what incentive you’re using, how frequently, what content you’re showing, what action you want them to take, and how you’re measuring whether it worked.

Today we can go much further. We can monitor in real time which feature each user is engaging with, build segments automatically and predictively. For example, identifying which users are likely to make their next payment and which are likely to miss an installment. From there, we act differently: for the user at risk of delinquency, we send payment prevention campaigns, while for the on-time payer we might offer a credit line increase. Same company, same users, completely different journeys.

I was recently at Fintech Americas, and the mantra everywhere was “we need to personalize with AI.” And at the same time, Braze’s 2026 Global Customer Engagement Review shows there’s a 40% gap between what companies believe they understand about their users and what users actually feel. Closing that gap takes more than dashboards. It means turning available data into concrete action at the right moment.

And the impact of closing it is measurable: when brands accurately predict user needs, consumers are 30% more loyal, 29% more likely to engage with brand content, 26% more likely to recommend it, and 23% more likely to make a purchase.

What the numbers say

Davivienda replaced its SMS strategy with a cross-channel approach built on personalization, automation, gamification, and AI. The result: 2.7x in transaction frequency, 3.7x in activity on their virtual store, and 40% faster experimentation and testing.

Stone incorporated systematic experimentation with Amplitude Experiment. They validated more than 50 experiments, ran more than 100 A/B tests per month, and executed 150 monthly rollouts. The impact on ARPAC: +5.97%.

Rappi moved from manual campaigns to automated, personalized segmentation. Results: +10% in first orders, -30% in acquisition cost, and 2.5x higher retention for users in their Prime program.

Capital One used Braze AI Decisioning to identify more than 113 user characteristics and send campaigns on the best day of the week for each individual. A single campaign delivered a 92% conversion rate and $16 million in additional revenue.

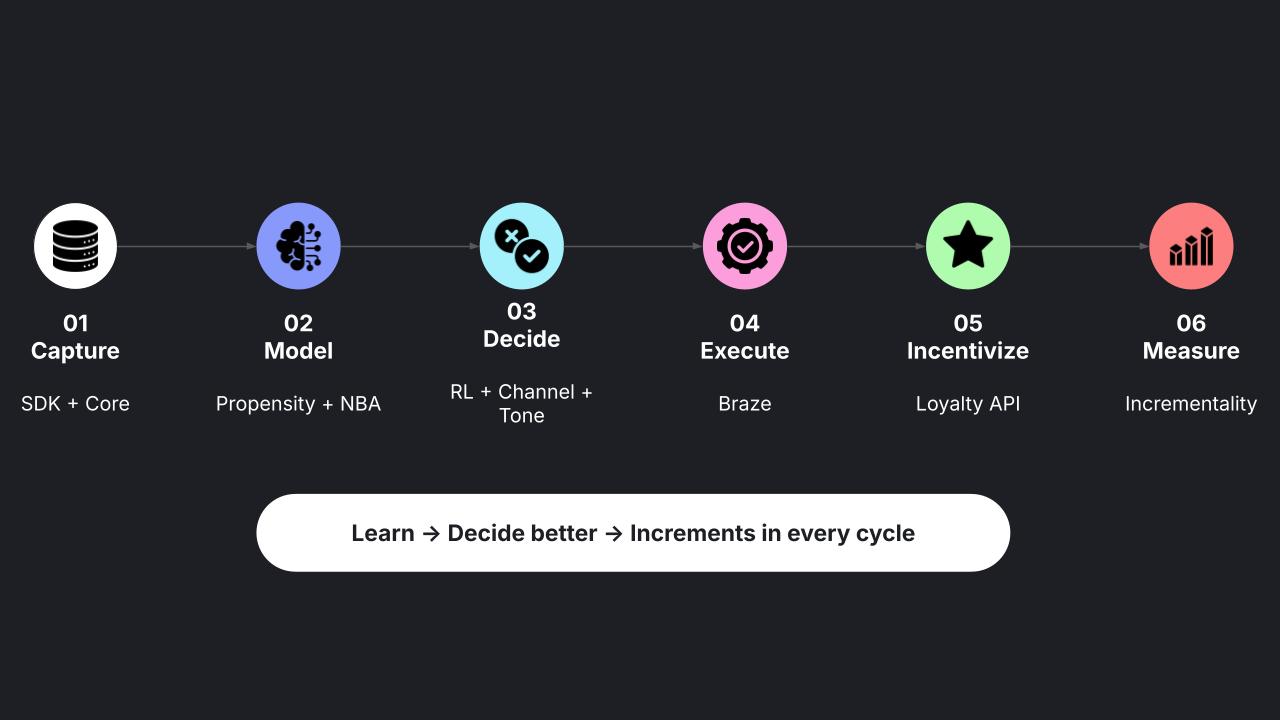

The loop that runs through all of it

Behind these results is a replicable architecture.

It all starts by capturing behavioral data from the front end (via SDK and core data) with the right level of granularity. Without this foundation, any model you build on top of it will have problems. We can use AI to optimize, but it’s useless without well-structured data.

On top of that data, you build models: propensity, next best action, risk, LTV. Those models generate scores that sync as attributes into execution platforms and those are what enable the next decision: which channel to use to reach the user, at what moment, and with what tone.

With that defined, you run the campaigns. Then comes the next layer: incentivizing based on who the user actually is. Not everyone deserves the same incentive. The question is whether it’s worth investing more or less in each person, and how to optimize that incentive to maximize incremental return.

Finally, you measure. Always with incrementality as your north star, always trying to understand which action or experiment actually generated real impact.

That loop, repeated with discipline, is what turns data into decisions and decisions into real growth.

Five pillars behind every use case

For that loop to work in practice, at Minders we operate around five pillars that are present in every successful implementation:

Technical architecture. A semantic layer with a single, unified conversion definition applicable across all systems — the foundation that lets every team measure with the same logic.

Marketing Science. Propensity, risk, LTV, and next best action models that sync as attributes into execution platforms.

Behavioral Science. The EAST framework, Kahneman’s principles (loss aversion, present bias, endowment effect), and neuroscience applied to incentive design. Understanding how users make decisions is a core part of the work.

Proven interface patterns. More than 14 patterns validated across 610+ A/B tests with more than 127 million visitors: social proof, benefits button, progressive participation, status visualization.

Experimentation and gamification. Every campaign has a control group and incremental revenue measurement — real business metrics, not opens or clicks. Gamification, when implemented with intention, is a genuine retention strategy: it guides users to discover new features, builds habit, and keeps them coming back.

From retention to revenue

Habit is won by measuring what matters, experimenting with rigor, and personalizing with intention. It’s a slow, disciplined, and measurable process and it’s the only one that produces primacy in a sustainable way.

At Minders, we’ve worked with more than 100 clients across Latin America, over 70 of them in the financial sector. With all of that accumulated experience, we decided to systematize it into 27 use cases for payments, credit, and investments. Each one includes the problem we identified, the hypothesis we tested, and the expected result if you implement it. They’re built around everything described here. The idea is that, with whatever stack you have, you can start thinking about what you can implement and begin generating more frequency, more retention, and more revenue from your users.

If you want to know which use cases to implement to start building primacy in your product, calculate the impact here.